Societatea Nationala Nuclearelectrica S.A. (“SNN”) published the convening notice for the General Meeting of Shareholders scheduled for 09.12.2016 which includes the proposal to renew the mandates of six current Board members of SNN, in compliance with the provisions of OUG 109/2011 regarding corporate governance of public companies, as subsequently amended (“OUG 109/2011”). The reasons for this proposal are presented in the explanatory note published on SNN’s website related to this item on the agenda of the OGMS, and the information and supporting data are available in the Activity Reports of the members of the Board of Directors whose mandates are proposed for renewal, drafted, in compliance with legal provisions. All these information is available in the Investors Relations section.

Any shareholder of SNN has the right and frequently the legitimate interest to support and oppose different views from those of the current Board of Directors, but, for a correct information of the public and shareholders, SNN considers it to be extremely important that the information disseminated in the media be presented in an objective manner focused on concrete facts and data, as opposed to subjective interest.

The dissemination of information in the public space which lead to a negative perception of the issuer, without supplying explanations for the causes, is a form of opposition towards a mere proposal subjected to the vote of the shareholders which doesn’t appear compatible with the status of a significant shareholder such as Fondul Proprietatea (“FP”).

Apart from the responsibility to protect the interests of its shareholders, regardless of the market context, SNN is and remains a national company, a strategic company, a Romanian company whose current major investment projects provide both short term benefits as well as long term benefits for its shareholders.

The public pressure exercised by the monitory shareholder for the orientation of SNN’s business strategy towards short term profits, without consideration for long term objectives and nuclear safety requirements is not compatible with any issuer especially a nuclear power producer. Nuclear power sector must be understood from the inside – the pillar of the nuclear sector is nuclear safety; this is what SNN and also international organizations such as IAEA and WANO and national ones (CNCAN) state.

FP stated publically on several occasions that it is interested in the maximization of the gains for the shareholders, and starting from this premise, it constantly opposes any long term project of the company, especially Cernavoda NPP Units 3 and 4 project, stating that this project would diminish the shareholders gains. Although, the strategy for the development of the project clearly states that the two units would bring considerable income for SNN through the capitalization of the existing assets which currently don’t generate any income, operation revenues based on an O&M contract, nuclear fuel supply revenues and dividends, revenues which undoubtedly will be reflected in the shareholders gains, FP had never publicly presented any data related to their position. SNN argues that Cernavoda NPP Units 3&4 project represents a healthy development solution for the company with long term benefits.

One of SNN’s Board members was appointed at the proposal of FP. Thus, FP had the opportunity to present proposals and growth strategies for SNN, either directly or indirectly.

The inly proposal of FP has been constantly the same one, namely the cancelation of Cernavoda NPP Units 3 and 4 Project. This proposal was never grounded on potential benefit analysis versus potential losses resulted from the cancelation of the project. At the same time, we wat to believe that despite the fact that FP hold interests in many energy companies, including companies which rely on different types of fuel to generate electricity, their point of view is not influenced by possible diverging interests related to the different participation in companies in the same sector, some of them in competition.

We remind the fact that the strategy for the continuation of Cernavoda NPP Units 3 and 4 project was approved by SNN GMS and by the Romanian Government and that the project was declared a strategic one by CSAT and is also at the top of the list of the future national energy strategy. The majority shareholder of SNN is the Ministry of Energy, and the management of the company carries out the mandate granted by the shareholders within the GMS. Within the GMS, the strategic decisions regarding investment projects are approved with a majority of the votes.

Thus, for a correct and accurate information of the public, with all the data needed for a fair opinion and these complex issues, SNN makes available to the public and the shareholders the following information, structured based on FP’s statements, from cause to effect.

- The energy market

SNN is an energy producer, with a constant production capacity, limited to cca. 1.400 MWh installed capacity by the technical characteristics of the two operating units; thus, the production cannot be increased in order to compensate the major energy price decrease during 2013-2016.

SNN is already operating at the highest standard of nuclear excellency which implies a capacity factor already above the average in the nuclear industry which places the two units on the top positions worldwide, thus the increase in the net production of the operating units is not possible. The decrease of production, however, is possible if SNN doesn’t take the adequate operation and maintenance measures, doesn’t ensure the necessary investments to maintain the operating capacity considering the natural wear of the units.

At the same time, the management is constantly considering long term objectives, even if this means the renunciation to short term results: an example is the decision to perform a major investment work during the planned outage of Unit 1 in 2016, with benefits on the long term for the shareholders, which required an extended outage period of an extra 20 days, and thus decreased production and revenues in 2016 but with benefits in the following period due to avoiding a future production decrease caused by the reduction of the thermal transfer performance. This is an eloquent example which indicated the compliance to the nuclear industry best practices which can be comprehended by anyone willing to do so. There are countless examples in the nuclear industry, when delaying certain investments out of the management’s selfish interest to cash in short term profits lead to disastrous consequences. Possible the investors were satisfied, but jeopardizing future results.

In order to comprehend the influence of the market on the producers, we state that until the complete liberalization of the energy market which will take place in 2017, the company sells its entire production on two market segments:

- The regulated market where the quantity and the prices are established by ANRE (the price being determined on the basis of economical justified costs plus a maximal regulated profit ratio); the percentage sold on the regulated market decreased constantly, due to the gradual liberalization of the market, from 50% in 2013 to 14% in 2016 while the price for 2016 decreased well below the price on the competitive market;

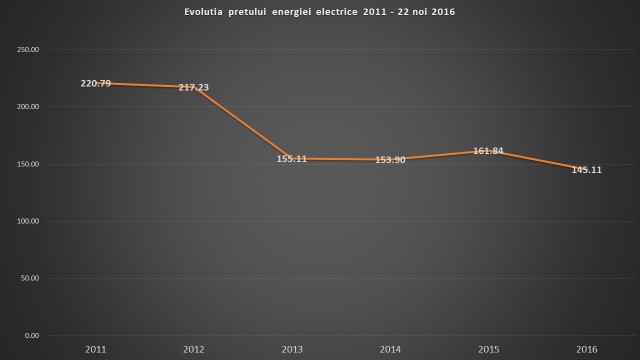

- The competitive market (the free market) where the prices have registered an accelerated decrease starting with 2013, reaching historical minimum levels registered in the last 8 years during the first 9 months of 2016. Thus, the average prices (with Tg) on the competitive market starting with 2011 up to present are the following:

- 2011 – 220,79 lei/MWh

- 2012 – 217,23 lei/MWh

- 2013 – 155,11 lei MWh

- 2014 – 153,90 lei/MWh

- 2015 – 161,84 lei/MWh

- 2016 (current date– 22.11.2016) – 145,11 lei/MWh

The chart indicated the decrease of the average prices on the competitive market (Tg included)

SNN is a majority state owned company, which, as per the provisions of the energy Law, is obliged to sell all its available production on the Romanian energy market (with the exception of the energy sold on the regulated market, where the price is out of the management’s control), where the price is established by the request and offer ratio. SNN’s management constantly publicly supported and requested the correction of the market failures in order to allow conventional producers such as SNN to capitalize their production by implementing certain measures for ensuring a functional, flexible and competitive market.

Moreover, SNN considers that the fair assessment of the company’s results is possible only by analyzing the market context, revenues, and profit which results mainly from the sale of electricity.

We are convinced that SNN’s shareholder FP is familiar with these market aspects or that it can easily verify them by requesting an analysis from energy market specialists. In this context, SNN considers that in order to maximize the efforts of the company’s management to correct market failure and implicitly, to increase the revenues of the company, FP needs to adopt a similar positioning, considering FP’s constant cause: the increase of the shareholders gain.

In the current market frame, a correct approach towards the issuer and the shareholders would be a policy supporting the efforts of the company’s management to promote legal changes in the benefit of SNN. Practically, FP as a legal person shareholder with a large exposure on Romania’s energy market, could have supported together with SNN, to the benefit of the shareholders, the following efforts:

- The annulment of the export interdiction which discriminates the Romanian energy producers in comparison with the competition in neighboring countries and the energy traders;

- The adjustment of the energy transport tariff, which is currently differentiated on geographical regions and which has the highest cost for the Dobrogea region, placing SNN on a disadvantageous position compared to other producers in different areas;

- The change of the legislation considering the fact that SNN is owner of a production and a supply license but faces difficulties in the interpretation of the legislation regarding the supply of electricity to end consumers. On one side (as a producers), Nuclearelectrica is obliged to sell the entire available quantity on the centralized market, and on the other side (as supplier), Nuclearelectrica has to right to supply energy. Energy supply also involves personalized offers towards end consumers, which contradicts SNN’s obligation as producer;

- The reduction of excessive regulations which make it impossible to ensure the continuity of sales during the outage periods;

- The correction of market failures such as: Day Ahead Market which was a quota of over 50% out of the total forecasted consumption, being a main market and not a marginal one as it was designed to be; the green certificate trade mechanism which put direct and unjustified pressure on the trading price of clean energy, thus affecting the formation of the price on this market segment and consequently the rest of the market etc

- The increase of the flexibility of the mechanism and platforms used by producers to trade their energy, which at present are extremely difficult and affect the liquidity of the market.

- The profitability of the company

The market context characterized mainly by the massive decrease of energy prices has a significant impact on the negative financial result of the company, the largest share of SNN’s revenues being generated by energy sales. SNN developed new energy sale strategies adopted to the new market context, SNN’s energy sale prices resulted from the sale of energy being constantly above the average market price, thus, the necessary internal measures for partially counteracting the price decrease were adopted, implemented and with optimum results compared to the market context, but insufficient to offset the major price differences between 2012 and 2016.

FP refers to the decrease of the profit during 2014-2015 after the historical profit obtained in 2013. In order to have a clear view of the evolution of the net profit during 2013-2015, considering the price decrease, it is necessary to present the comparison to the year prior to 2013-2015 period.

We present below the net profit reported by the company starting with 2011 (extracted from the consolidated financial statements IFRS for 2011 and IFRS-EU for 2012 and beyond, rounded to million lei):

- 2011 – net profit 83 mil. lei.

- 2012 – net profit 20 mil. lei

- 2013 – net profit 427 mil. lei

- 2014 – net profit 131 mil. lei

- 2015 – net profit 147 mil. lei

The profit for 2013 is explained also by the fact that most of the energy sale contracts were concluded on the competitive market in 2012 when the market prices were much higher, thus the revenues reflected in the profit for 2013, accordingly; at the same time, considering the fact that the prices decreased abruptly in 2013 compared to 2012, many buyers terminated the contract signed in 2013, opting to pay the contractual penalties and assuming the risk of being summed to trial. Thus, a significant portion of the revenues came from penalties. Moreover, in 2013 a significant positive net financial result was registered, based on favorable net currency exchange differences, which in turn influenced the net profit of the company.

Thus, judging solely on the premises that the role of the current Board of Directors is the increase in the profitability of the company, then, from this point of view, one can clearly notice that in the period prior to 2013, characterized by high energy process, the related net profit for the period 2013-2015 increased, although the differences in the energy prices are significant.

The decrease of the profit during 2013-2015 reflects mainly the decrease of the market price, a clear dependence correlation existing between the two. FP’s statement regarding the decrease of the profit during this period does not present any causes and does not permit a comparison with the previous years in order to position the results of the current Board of Directors compared to the previous status of the company, before their mandate. A fair and objective assessment can be performed only in correlation to the previous period and to the market.

At the same time, the financial results were affected by sudden fiscal changes (the tax on special constructions, the tax on non-resident buildings in 2016 due to the elimination of the exception for nuclear power plants), tax and obligations that the management of SNN and any other energy producer cannot control and absorb. SNN didn’t notice any constructive positioning from FP in this context, either.

Regarding the measures taken for cost control, we make the following statements.

- Capital market

Starting with November 2013, SNN is listed on Bucharest Stock Exchange, during the first year of the mandate of the current Board of Directors. SNN’s shareholding structure is as follows: The Romanian State through the Ministry of Energy: 82,49%, the Property Fund 9,09% and other shareholders 8,41%.

SNN’s listing price was of 11,2 lei/share. From the time of the listing up to present, the share price decreased with over 50%, the main reasons being:

- The different market context. Previous to the listing, as shown above, the higher energy prices, could have potentially influenced the expectations of investors regarding their continuity in the years to follow; no fiscal changes were anticipated at that time such as the taxation of buildings with great amounts of money, thus the financial results corresponded to the decrease of the energy price and the impact of the above mentioned taxes, which lead to a decrease of the share’s price.

- Objective factors in the assessment of the issuers by legal person shareholders due to the fact that SNN are a reduced capitalization and free-float which has an impact on the interest of investors and investment funds, most of them having very high value thresholds for investment decisions; the characteristics of the Bucharest Stock Exchange are added to this, as well as the general evolutions in the sector.

SNN’s share price and be increased, in SNN’s opinion by applying the following methods, which are constantly on the agenda of the management team:

- The correction and modification of the legal framework in order to ensure a better operation of the energy market and to allow the company to increase its revenues, by submitting proposals to the relevant decision makers in Romania;

- Diversification by involvement in projects that yield SNN additional revenues and added value, objectified by the intention of the current Board of Directors to purchase a part of the assets of a certain energy distributer in Romania;

- A plan for the diversification of activities in order to use the supply license of SNN, in compliance with the applicable legislation

- Development of the company’s projects, including the successful implementation of Units 3 and 4 Project which represents a viable development direction for SNN.

Thus, FP’s accusation that the management did not performe any action to increase the price of the shares is ungrounded, moreover due to the fact that FP is well aware of these efforts.

- Cost efficiency

The actual figures of the operating expenses (adjusted*) during 2012 – 2015 are as follows:

- 2012: 1.051.568 thousand lei

- 2013: 1.066.424 thousand lei

- 2014: 1.015.916 thousand lei

- 2015: 993.332 thousand lei

*) Note: for an adequate comparison, the operating costs are presented without the costs for depreciation and amortization, the costs for energy transport (which are included in revenues) and the cost for the tax on special constructions for 2014 and 2015.

A decrease of the operating costs can be noticed which was possible without affecting nuclear safety which is the absolute priority. No nuclear power operator will ever approve the intentional decrease of the costs up to the point that these decrease can affect nuclear safety and no shareholder of a nuclear power producer, knowing its specific, would ever request the decrease of the operating costs thus affecting nuclear safety. SNN is a nuclear power operator, industry which implies strict legislation, norms and standards applicable at the international and national levers as well as an economic operator, applying specific market regulations. For integrated results, both conditions must be met by finding an optimum balance between the operating and production component and the financial and economic one.

We must not forget the fact that operational performance can be reached only with the adequate human resource, not only the financial one. In this context, the human factor has a decisive contribution to reaching this performance and must be remunerated accordingly, stimulated to deliver the same performance in the future and retained within the company; such a policy requires adequate resources, and the results in the previous years show that nuclear excellence in the operation of Cernavoda NPP Units 1 and 2 was achieved without a significant increase of the personnel remuneration. The management and the shareholders must be constantly aware of the specifics of the nuclear industry.

- The remuneration of the management

The annual reports of the Nomination and Remuneration Committee are public since 2013 up to present, comprising all the information regarding the remuneration earned by the members of the BoD, the General Manager, the Manager of CNE Cernavoda Branch and the Financial Manager and, during this entire period the structure of the remuneration of the executive and non-executive BoD members remained unchanged. There is increase in the total value of the remuneration of the BoD members and of the executive management in 2014 and 2015 compared to 2013, the perceived difference in value resulting from the mere fact that in 2013, there were only 8 months of mandate contracts paid compared to 12 months in the next years. Also, the category management remuneration presented in the financial statements includes other persons with management positions (employees), who don’t have mandate contracts concluded with the company.

The performance indicators are assumed through the mandate contract and their update based on the annual budgets is natural as the annual budgets are planned precisely to anticipate and control the complexity of the operational and production needs, of the investments, the market, especially since the market is highly dynamic and unstable. We underline the fact that the correlation of the indicators with the annual budgets is provided in the mandate contracts approved by the shareholders as a possibility. This is the rational and responsible approach without implying a modification of the performance indicators. As one can notice from the results for the first semester of 2016, the degree of achievement of the performance indicators is correlated with the actual results, and the remuneration paid as a consequence (the remuneration for the second quarter for the variable component was adjusted as per the provisions of the mandate contracts). All these information is public and FP had access to it.

- The refurbishment of Cernavoda NPP Unit 1

The refurbishment of Cernavoda NPP Unit 1 is a distinctive project than Units 3 and 4 project, a certain project of SNN approved the GMS in 013 and under planning phase. In order to have an accurate value estimate of the refurbishment costs, technical analysis of equipment is needed as well as a clear image of the maintenance/procurement needs, to which the cost of the works is added. As per the internal action plan, the technical analysis will be completed at the end of 2017. The financing structure is a mixt one: internal sources and external sources, and the contracting of external sources will take place after 2017. Considering the fact that the contracted loans for the completion of Unit 2 will be fully reimbursed until 2024, the indebtedness of SNN will be at a good level, remaining to demonstrate the financial feasibility of the project and the capacity to reimburse the loans, namely to generate profit for the shareholders following the refurbishment.

Considering the fact that the two projects are different as approach and investment, we inform FP that a fund transfer from Units 3 and 4 project to the refurbishment of Unit 1 project cannot be performed, and as a consequence, the effort invested in Units 3 and 4 project does not impede the continuation of the activities for the refurbishment of Unit 1, started in 2013.

- The renewal of the mandate contracts for the BoD members

Within the GMS of 09.12.2016, the shareholders will be asked to approved the renewal of the mandate of the 6 members of the BoD. Regarding FP’s statement that the BoD of the company convened the GMS although one of the members of the Board (Mr. Codrut Bogdan Nicolae Stanescu) was not selected in compliance with the provisions of OUG 109/2011 and that the provisions of art. 28 paragraph 5 of OUG 109/2011 are not met, we make the following arguments:

- Each member of the Bo Dis entitled to the renewal of his mandate contract, as per the provisions of OUG 109/2011 and, from this perspective, it is the exclusive right of the shareholders to decide regarding this aspect in compliance with the legal provisions. SNN presented to the shareholders all the information necessary to reach a decision on the matter: each member of the BoD presented an activity report, their CVs, the information note to the shareholders presented the correct information, the criteria which must be considered on electing the BoD members; thus, the shareholders will decide, as per their legal competence, on the items included on the agenda, regarding the renewal of the mandate contracts which expire on 25.04.2017;

- SNN’ BoD acted prudently and diligently by convening the general meeting of shareholders in order to discuss the renewal of the mandate contracts that expire on 25.04.2017, expressly mentioning in the note presented to the shareholders, that in case the shareholders don’t approve the renewal of the mandate contracts, a selection procedure can be organized as per the provisions of OUG 109/2011, with enough time for the initiation, unfolding and completion of the procedure within the legal term of 4-6 months;

- As per the provisions of art. 28 paragraph 1 of OUG 109/2011, the mandate of the administrators who fulfilled their objectives can be renewed following an evaluation process;

- Provisions of art. 29 paragraph 14 of OUG 109/2011 states that, in case the candidates proposed for the BoD are current administrators, the request for the renewal of the mandate are addressed to the general meeting of shareholders.

- The mandate of the general manager

With regards to the mandate of the General Manager, in the note presented to the shareholders, the BoD did not mention, contrary to FP’s argument, the fact that the renewal of the mandate of the members of the Bo Dis equivalent to the renewal of the mandate of the General Manager of the company, but, transparently stated the in case the shareholders approve the renewal of the mandate of the current administrators, the mandate of the General Manager will be renewed as well for a period of 4 years, considering the fact the she fulfilled its performance indicators. Moreover, contrary to FPs statements, the GMS will not be requested to approve the renewal of the contract of the General Manager, which can be easily noticed by reading the agenda of the meeting, because such a decision is in the competence of the BoD and not of the shoulders.

The General Manager was appointed following a selection procedure organized on the basis of OUG 109/2011. Thus, the renewal of the mandate contractual of the General Manager does not contradict the provisions of art, 35 paragraph 4 due to the fact that the General Manager was selected based on the provisions of OUG 109/2011. We consider it to be absurd to qualify that the intention of the law makers was to select a new General Manager at each 4 years, regardless the achievement of the performance indicators and of the need to ensure stability and continuity. Moreover, as per the mandate contract, the principal always has the right to renew the mandate contract of the representative if he considers that the representative fulfilled his obligations accordingly, this being provided as an option on the mandate contract of the general manager.